Between 2020 and 2024, something fundamental shifted in how Americans access real estate investments. Properties that would’ve required $50,000 checks and country club connections now accept investments as small as $100. The catalyst? Blockchain technology applied to property ownership.

Today’s tokenization platforms let a dental hygienist in Kansas City own a sliver of a Brooklyn apartment building. That same week, a freelance designer in Portland might pick up shares in a Dallas warehouse. No property management headaches. No middle-of-the-night maintenance calls. Just fractional ownership recorded on distributed ledgers.

Why does this matter? Three barriers have kept most Americans out of direct real estate: you need serious capital upfront, selling takes forever, and you’re typically stuck investing wherever you happen to live. Tokenization cracks all three problems wide open.

What Is Real Estate Tokenization?

Here’s the basic mechanism: ownership stakes in buildings get divided into blockchain-based digital tokens. Think of it like slicing a pizza into hundreds or thousands of pieces, where each slice gives you a proportional claim on the whole pie.

The technical setup usually works like this. A property owner or sponsor creates a limited liability company that takes legal title to the real estate. That LLC then issues digital securities—tokens—representing membership shares. Buy tokens, and you own a piece of the LLC. The LLC owns the building. Therefore, you own part of the building. The blockchain simply tracks who owns which tokens.

Traditional property ownership means filing paperwork at your county recorder’s office, waiting for stamps and signatures, storing physical certificates. Digital ownership flips that model. Your tokens sit in a software wallet. The blockchain (often Ethereum or Polygon, sometimes private networks) serves as the master record. When you sell tokens, smart contracts execute the transfer automatically without title companies or escrow agents slowing things down.

We’re solving a problem that’s existed since medieval land registries—how do you make property as easy to divide and trade as paper stocks while keeping the legal protections intact? Blockchain doesn’t replace property law. It makes enforcing and transferring those rights dramatically more efficient.

Michael Chen

Beyond just tracking ownership, smart contracts handle the boring administrative work. A building generates $100,000 in monthly rent? The smart contract automatically calculates each token holder’s share and deposits it into their account. Thousands of investors get paid the same day without anyone cutting checks or updating spreadsheets. Everything’s transparent—you can verify the math yourself on the blockchain.

How Real Estate Tokenization Works

Bringing a building onto the blockchain involves several distinct phases, each balancing innovation against regulatory requirements.

Choosing and Vetting Properties: Tokenization platforms start by identifying buildings that make sense for fractional ownership. Stabilized, income-producing properties work best—think apartment complexes with steady tenants, not speculative land deals. A strip mall with established leases and predictable cash flow? Perfect. A ground-up condo development in a risky market? Not ideal. The sponsor runs standard real estate due diligence: inspections, title searches, environmental reviews, financial audits. Nothing gets tokenized before passing the same scrutiny as traditional acquisitions.

Setting Up Legal Structures: The property transfers into a special purpose vehicle—almost always an LLC or Delaware Statutory Trust created solely to hold that one asset. Lawyers draft offering documents meeting SEC requirements. Most deals use Regulation D (Rule 506b or 506c) for private placements to accredited investors. Larger offerings sometimes use Regulation A+, which allows non-accredited investors but requires more disclosure and SEC review. These documents spell out who can invest, what risks exist, and what ongoing reports investors will receive.

Building Smart Contracts and Minting Tokens: Development teams write and deploy smart contracts on their chosen blockchain. The contract defines total token supply, transfer restrictions, and automated functions like rent distributions. Say you’re tokenizing a $10 million office building. You might create 10 million tokens at $1 apiece—each representing 0.00001% ownership. (Though many sponsors use different math to avoid fractional cents.) The smart contract enforces securities compliance automatically: blocking transfers to unqualified buyers, implementing holding periods, preventing sales that would violate offering terms.

Opening Investment to Participants: Once the offering goes live, investors create platform accounts, verify their identity (government ID, address confirmation, sometimes facial recognition), and prove accredited investor status if required—tax returns showing $200,000+ income, brokerage statements with $1 million+ net worth excluding your home, or verification letters from CPAs. After approval, you fund your account via bank transfer or crypto and purchase tokens. They appear in your platform wallet within hours or days, depending on the offering structure. Rental income starts flowing to your account based on your ownership percentage.

Enabling Secondary Market Trading: This is where fractional ownership on blockchain shows its advantage over traditional syndications. Rather than waiting five to ten years for the sponsor to sell the property, some platforms run secondary marketplaces. Want to exit your position? List your tokens for sale. Another qualified investor sees your listing and buys. The transfer happens through smart contracts, maintaining compliance throughout. Liquidity quality varies wildly—a Manhattan commercial building might trade weekly while a rural warehouse sees one transaction per quarter.

Leading Real Estate Tokenization Companies in the US

Several platforms have established themselves with track records, regulatory frameworks, and actual properties generating returns.

RealT concentrates on residential rentals primarily in Detroit, Chicago, and nearby Midwest markets. Their distinguishing feature? Extremely low entry points—some properties let you invest for under $100. They tokenize on Ethereum, pay weekly rental distributions in stablecoins (USDC), and target both accredited and non-accredited investors through various exemption structures. The platform emphasizes transparency, publishing property addresses, financial details, and even renovation photos.

Securitize Markets operates differently from most competitors. They don’t originate deals themselves. Instead, they’ve built a registered Alternative Trading System—a regulated secondary marketplace for digital securities including real estate tokens. Real estate sponsors partner with Securitize to tokenize their properties, then investors trade those tokens on Securitize’s ATS. The regulatory infrastructure includes broker-dealer registration and integration with traditional banking systems.

Elevated Returns focuses on trophy assets in the luxury hospitality sector. Their landmark deal tokenized equity in the St. Regis Aspen Resort, marking one of the industry’s most high-profile transactions. The emphasis on premium properties means higher barriers to entry—typically $10,000 minimum investments and accredited investor requirements. Returns target investors seeking exposure to established, institutional-grade assets rather than speculative plays.

RedSwan CRE built a marketplace model for commercial properties. Real estate sponsors and property owners list tokenized offerings across office buildings, shopping centers, and industrial facilities. The variety creates more selection but also more variability in quality and terms. Minimum investments generally start around $5,000 for accredited investors, with specific requirements varying by deal.

Slice (previously operating as Slice Capital) concentrates on single-family rental homes and smaller multifamily properties. Their strategy emphasizes geographic diversification—spreading investments across multiple metros to reduce concentration risk. The platform manages properties through third-party operators, maintaining the passive investment experience. Minimums typically run $10,000 for accredited investors.

| Company Name | Minimum Investment | Property Types | Accreditation Required | Liquidity Options |

|---|---|---|---|---|

| RealT | $50–$150 | Residential (single/multifamily) | Usually no | DEX trading, peer-to-peer sales |

| Securitize Markets | Deal-dependent | Residential, commercial, mixed | Yes | Regulated ATS with broker-dealer oversight |

| Elevated Returns | $10,000+ | Luxury hospitality, premium commercial | Yes | Limited secondary trading |

| RedSwan CRE | $5,000–$25,000 | Office, retail, industrial | Yes | Platform-based marketplace |

| Slice | $10,000 | Single-family, small multifamily | Yes | Quarterly redemption windows |

These platforms reflect different philosophies. Some maximize accessibility with tiny minimums and open eligibility. Others curate institutional-quality deals with higher thresholds but potentially more stability.

Benefits and Risks of Tokenized Real Estate Investment

Key Benefits

Dramatically Lower Entry Points: Traditional real estate syndications demand $25,000 to $100,000 just to get in the door. Tokenization drops that floor. Some platforms accept under $100. A new investor with $5,000 can build a diversified basket across five properties in different markets instead of concentrating everything in one REIT or crowdfunding deal. You’re assembling a portfolio that would’ve required $100,000+ a decade ago.

Actual Liquidity Improvements: Yes, real estate remains fundamentally illiquid compared to Apple stock. But tokenization creates exit options that traditional syndications never offered. Instead of waiting seven years for a property sale, you might list tokens on a secondary market and find a buyer in two weeks. Liquidity quality varies enormously—popular properties in major metros might trade with 2-5% bid-ask spreads while secondary assets sit for months. Still beats waiting for the sponsor’s exit timeline.

Transparency You Can Verify Yourself: Blockchain’s public ledger means every transaction lives in the open. Smart contracts automate rent payments on predetermined schedules—no wondering when distributions hit or whether management “forgot” this month. Platform dashboards pull data directly from property management systems, showing real-time occupancy, maintenance expenses, and financial performance. You’re not relying solely on quarterly reports.

Geographic Flexibility: An investor in San Francisco can own pieces of properties in Austin, Nashville, Miami, and Phoenix without stepping on a plane. This spread reduces exposure to regional downturns—California’s tech recession doesn’t tank your entire portfolio if half your holdings sit in Texas and Florida. Traditional investors needed either enormous capital or complex REIT structures to achieve similar diversification.

Cutting Out Middlemen: Traditional real estate transactions feed an army of intermediaries. Brokers, title companies, escrow agents, transfer agents—everyone takes a cut. Smart contracts reduce (though don’t eliminate) these costs. Automated distributions replace manual check processing. Blockchain-based transfers skip some traditional closing costs. The savings aren’t revolutionary but they’re real.

Potential Risks and Considerations

Regulatory Ground Keeps Shifting: Securities laws around digital assets continue evolving. A platform compliant today might face new requirements next year as the SEC refines its positions. Some platforms have received Wells Notices threatening enforcement. Investors might encounter unexpected restrictions on trading or additional compliance burdens. The legal landscape hasn’t settled into stable patterns yet.

Platform Dependency Creates Vulnerabilities: Your investment’s accessibility depends entirely on the tokenization company staying operational and competent. Platform shuts down? Marketplace closes? Technical failures? Accessing your investment becomes complicated fast. Unlike FDIC insurance protecting bank deposits, no government backstop covers platform failures. You’re trusting a relatively young company with potentially significant capital.

Short Track Records Mean Unknown Downturn Behavior: Most tokenization platforms launched after 2018. They haven’t weathered a severe real estate downturn or credit crisis. We don’t know how secondary markets function when everyone wants to sell simultaneously. Historical performance data spans five years maximum—barely enough to draw conclusions. How do these investments behave during recessions? We’re going to find out together.

“Liquidity” Doesn’t Mean “Instant Cash”: Despite improvements over traditional syndications, secondary markets remain thin. List tokens for sale and you might wait weeks or months for a buyer. Or you’ll need to discount 10-15% to move quickly. Popular properties in major metros trade more actively than secondary-market assets. The promise of liquidity exists in theory but its quality varies wildly. Don’t invest money you might need within 12-24 months.

Core Real Estate Risks Remain Unchanged: Tokenization changes how ownership gets recorded and transferred. It doesn’t change whether tenants pay rent, roofs leak, or markets crash. A tokenized apartment building faces identical operational challenges as any other rental property—vacancy, deferred maintenance, property taxes, insurance costs, difficult tenants. The blockchain doesn’t fix a broken HVAC system or market oversupply.

Tax Reporting Gets Complicated Quickly: Tokenized real estate generates K-1 forms reporting your proportional rental income, expenses, mortgage interest, and depreciation. Add passive activity loss limitations. Invest in properties across five states? Prepare for tax filings in five jurisdictions. Receive distributions in cryptocurrency? That creates taxable events at fair market value requiring cost basis tracking. Many investors discover at tax time that their $500 investment generates $200 in CPA fees.

How to Invest in Tokenized Property

Getting started means navigating both traditional investment procedures and blockchain-specific steps.

Research and Select a Platform: Match platforms to your goals, property preferences, and investor status. Read the full Private Placement Memorandum or Offering Circular—yes, all 80-150 pages. These documents contain crucial information about fees, risks, and financial projections that marketing materials gloss over. Compare fee structures carefully: annual management fees typically run 1-2%, with acquisition fees, disposition fees, and sometimes profit participation on top. Calculate total costs before committing capital.

Complete Registration and Verification: Account creation requires identity verification meeting KYC/AML requirements: government-issued ID, proof of address (utility bill or bank statement), sometimes facial recognition matching your ID photo. Accredited investor offerings require additional documentation—two years of tax returns showing $200,000+ annual income ($300,000 joint), or brokerage statements proving $1 million+ net worth excluding your primary residence. Some platforms accept verification letters from CPAs or attorneys instead of sharing financial documents directly.

Fund Your Investment Account: Most platforms accept bank wires or ACH transfers. Wire transfers process faster (1-3 business days) but cost $15-30. ACH saves fees but takes 3-5 days. Some platforms accept cryptocurrency deposits, introducing additional tax complexity since crypto-to-token purchases trigger capital gains calculations. Factor in timing—popular offerings sometimes close before your bank transfer clears.

Perform Property-Level Due Diligence: Study property financials, market analysis, and operator track records like you would any real estate investment. Key metrics: current occupancy rates, historical vacancy, debt-to-value ratio (under 65% preferred), cash-on-cash return projections (be skeptical of anything promising 15%+ annually in stable markets), and realistic exit timelines. Look for conservative underwriting. Compare projected returns against institutional investors’ targets for similar properties—if they’re targeting 8-10% and this deal promises 18%, question why.

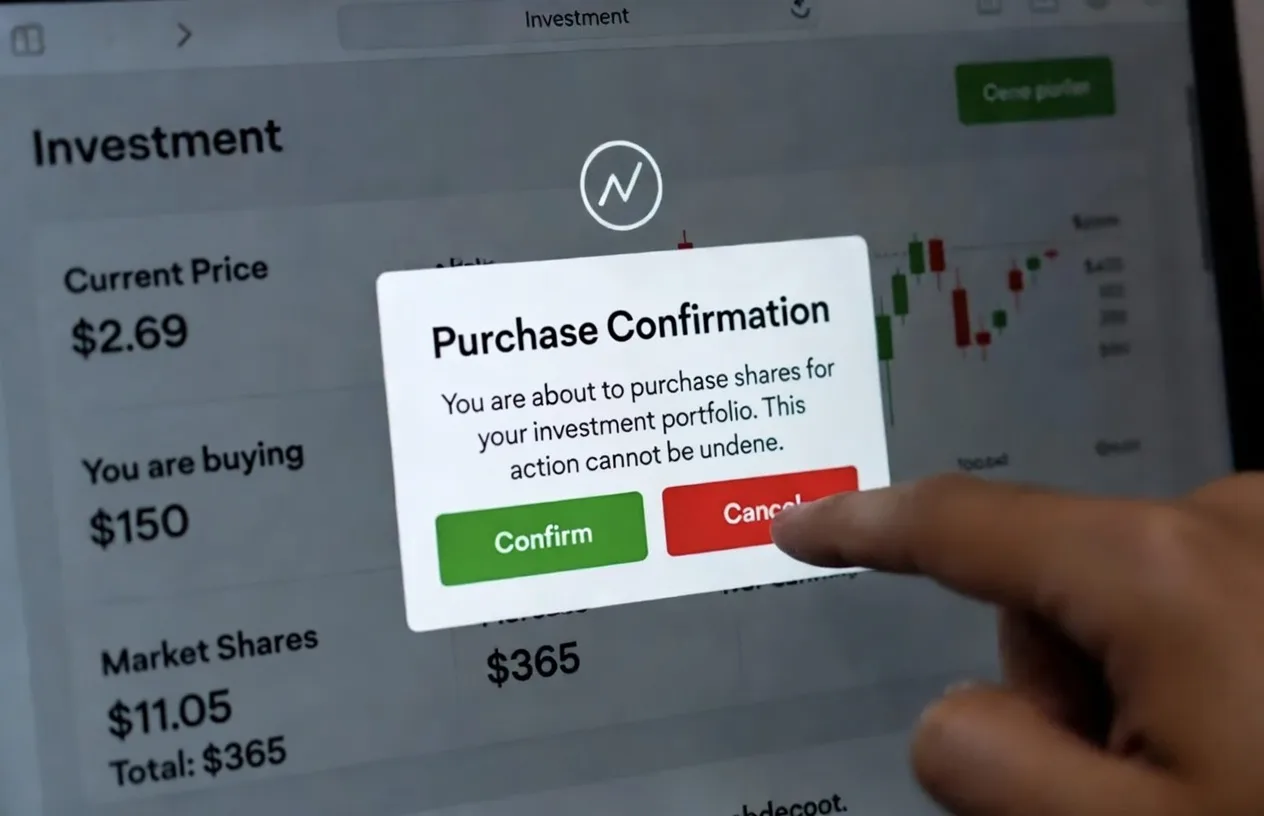

Execute Your First Transaction: Select the property and investment amount. Review the subscription agreement—this legal contract details your rights, obligations, and restrictions. Common provisions include holding periods before secondary trading, limitations on transfers, and dispute resolution through arbitration. Sign electronically and confirm your purchase. Tokens typically appear in your platform wallet within 24-72 hours after the offering closes and reaches its minimum funding threshold. Some platforms issue tokens immediately; others wait until the deal is fully funded.

Ongoing Monitoring and Portfolio Management: Track rental distributions through platform dashboards. Review quarterly or monthly property updates. Watch for maintenance issues, occupancy changes, or market shifts affecting property values. Decide whether to reinvest distributions or transfer cash to your bank account. If secondary trading is available, monitor token prices and trading volume to understand exit options. Don’t assume you can sell at par value instantly—track actual bid-ask spreads on comparable properties.

Common mistake worth avoiding: investing without understanding the holding period. Many offerings include 12-24 month lockups before any secondary trading is permitted. Even after lockups expire, finding buyers requires patience and potentially accepting discounts.

Regulation and Legal Framework for Real Estate Tokens

Real estate tokens fall squarely under existing securities laws, primarily enforced by the SEC. The agency applies the Howey Test to determine securities status, examining whether an investment involves money invested in a common enterprise with profits derived primarily from others’ efforts. Real estate tokens almost always meet this definition.

Securities Compliance Pathways: Platforms typically rely on Regulation D exemptions for private placements. Rule 506(b) allows sales to unlimited accredited investors plus up to 35 sophisticated non-accredited investors, but prohibits general solicitation or advertising. Rule 506(c) permits general advertising but restricts sales exclusively to verified accredited investors—no exceptions. Regulation A+ provides an alternative pathway for offerings up to $75 million, allowing sales to both accredited and non-accredited investors after SEC qualification and with ongoing reporting requirements similar to public companies.

Investor Protection Mechanisms: Registration requirements force issuers to disclose material information: property financials, operating history, risk factors, management backgrounds, use of proceeds, and conflicts of interest. Investors receive offering documents comparable to traditional real estate syndications, though some platforms provide more detail than required. Anti-fraud provisions prohibit misrepresentations and material omissions, with civil and criminal penalties. State and federal regulators can pursue enforcement actions against platforms making false claims or omitting crucial facts.

Secondary Trading Regulatory Requirements: Platforms operating secondary marketplaces face additional oversight. Operating an Alternative Trading System requires SEC registration and FINRA membership, subjecting the platform to examination, surveillance requirements, and ongoing compliance obligations. These platforms must implement market manipulation surveillance, maintain fair access for qualified participants, and file regular operational reports. Registration provides investor protections but limits platform flexibility—every feature requires regulatory consideration.

State-Level Complications: Real estate tokens may trigger state securities laws (blue sky laws) requiring registration or notice filings in every state where investors reside. Some states apply additional requirements beyond federal exemptions. Property ownership also subjects investments to laws in the state where the real estate sits: property taxes, landlord-tenant regulations, foreclosure procedures, and local ordinances. A tokenized property in California faces California property law regardless of where token holders live.

Tax Treatment Under Current Guidance: The IRS hasn’t issued specific guidance on real estate tokens, so tax professionals treat them like traditional partnership interests by default. Investors receive Schedule K-1 forms reporting proportional shares of rental income, operating expenses, mortgage interest, and depreciation. Passive activity loss rules typically apply, potentially limiting the ability to deduct losses against ordinary income. Receiving distributions in stablecoins or cryptocurrency creates additional complexity—each payment is a taxable event reported at fair market value on the receipt date.

The regulatory environment remains dynamic. The SEC has brought enforcement actions against platforms conducting unregistered securities offerings, emphasizing the importance of working with compliant platforms that prioritize regulatory adherence over aggressive marketing claims.

FAQs

Minimums span from under $100 to $25,000+ depending on which platform and property you choose. RealT operates at the accessible end—residential rental properties starting around $50-$150 per token, making it realistic for small investors building positions gradually. Platforms emphasizing commercial or luxury properties typically require $5,000-$25,000 minimums. Property type drives these thresholds partly—institutional-grade assets maintain higher minimums to avoid managing thousands of tiny accounts. A $50 million office building doesn’t want to track 500,000 investors holding $100 each. Administrative complexity becomes unmanageable.

Yes, the SEC treats the overwhelming majority of real estate tokens as securities subject to federal securities laws. This isn’t optional or debatable—it’s settled law under the Howey Test. Platforms must either register their offerings (expensive and rare) or qualify for exemptions like Regulation D or Regulation A+. This oversight provides crucial investor protections: disclosure requirements, anti-fraud provisions, and enforcement mechanisms when things go wrong. Platforms operating secondary markets may need broker-dealer registration or Alternative Trading System status. Before investing, verify that the platform has proper legal structure and compliance—check offering documents for SEC exemption citations and legal opinions.

Real estate tokens provide improved liquidity over direct ownership or traditional syndications, but you’re not getting anywhere near stock market liquidity. Secondary market activity varies dramatically. Popular properties in major metros might see weekly trades with 2-5% bid-ask spreads—meaningful liquidity that lets you exit without massive discounts. Other properties generate minimal trading volume. You might list tokens and wait months for buyers, or accept 10-15% discounts to sell quickly. Many offerings include 6-24 month lockup periods before any secondary trading is permitted. Consider tokenized real estate as medium-liquidity—easier to exit than a five-year syndication commitment but not convertible to cash on demand.

Depends entirely on the specific offering and which exemption the platform uses. Many tokenized real estate deals require accredited investor status (annual income exceeding $200,000 individually or $300,000 jointly, or net worth over $1 million excluding your primary residence) because they rely on Regulation D exemptions. However, some platforms structure offerings under Regulation A+ or other frameworks permitting non-accredited investors. RealT, for instance, offers numerous properties to non-accredited investors. Always check the offering documents for eligibility requirements before starting—eligibility is property-specific, not platform-wide.

Tokenized real estate investments generate tax treatment matching traditional partnership interests. You’ll receive Schedule K-1 forms reporting your proportional share of rental income, operating expenses, mortgage interest, depreciation, and capital gains or losses. Rental income is typically passive income subject to passive activity loss limitations—you might not be able to deduct losses against wage income. Selling tokens creates capital gains or losses reported on Schedule D. Receiving distributions in cryptocurrency complicates matters further—those payments are taxable events at fair market value requiring cost basis tracking for future dispositions. Multiple properties across different states potentially require tax filings in each state where property is located. Budget for CPA fees if your tokenized portfolio grows beyond one or two properties.

Blockchain technology provides robust security for ownership records through cryptographic methods that are extraordinarily difficult to forge or manipulate. The distributed ledger creates redundancy—thousands of nodes maintain copies, making it nearly impossible to alter records retroactively. However, security depends on multiple factors beyond blockchain itself. Your private keys must be protected rigorously—lose them and you’ve lost access to your tokens with no customer service department to call. Platform security matters separately; exchanges and marketplaces can be hacked, potentially exposing user credentials or funds held in custody. The legal structure connecting digital tokens to actual property rights must be ironclad, or the blockchain ownership might not be enforceable in court during disputes. Blockchain solves certain security problems elegantly while introducing new risks around key management and smart contract vulnerabilities that traditional property ownership doesn’t face.

Real estate tokenization platforms have cracked open property investment for investors who were previously locked out by capital requirements, illiquidity, and geographic constraints. The technology delivers fractional ownership, automated income distributions, and improved exit options while maintaining real estate’s fundamental economics.

The market has matured past early experimentation. Established platforms demonstrate regulatory compliance, deliver property returns, and operate functioning secondary markets. Investors can now assemble diversified real estate portfolios across property types and regions with capital that wouldn’t have qualified for a single traditional syndication five years ago.

Yet tokenization doesn’t eliminate real estate’s inherent characteristics. Properties still need management. Markets still cycle through booms and busts. Returns still depend on operator competence and economic fundamentals. Blockchain records ownership more efficiently, but it doesn’t make tenants pay rent or prevent recessions.

Success in this space requires traditional real estate diligence—understanding property fundamentals, evaluating operator track records, maintaining realistic return expectations—combined with new considerations around platform risk, evolving regulations, and blockchain technology. Investors who treat tokenization as an enhancement to real estate principles, not a completely novel paradigm, position themselves to benefit from the technology while avoiding speculative mistakes.

The platforms covered here represent current market leaders, but this space evolves rapidly. New entrants launch. Regulations clarify (or complicate). Technology improves. Staying informed about regulatory developments, platform changes, and market conditions remains essential for building a tokenized real estate portfolio that actually performs as expected.