When Bitcoin plunged from nearly $69,000 in late 2021 to under $16,000 by late 2022, over $2 trillion in cryptocurrency market capitalization vanished. Investors watched their portfolio values evaporate, prompting an urgent question: where did all that money actually go?

The answer challenges most people’s intuitions about how markets work. Understanding what happens during a crypto crash requires separating actual cash movement from perceived value changes—a distinction that explains why market cap can drop by billions while relatively little money actually changes hands.

How Cryptocurrency Gets Its Value

Before examining where value goes during a crash, we need to understand where crypto value comes from in the first place.

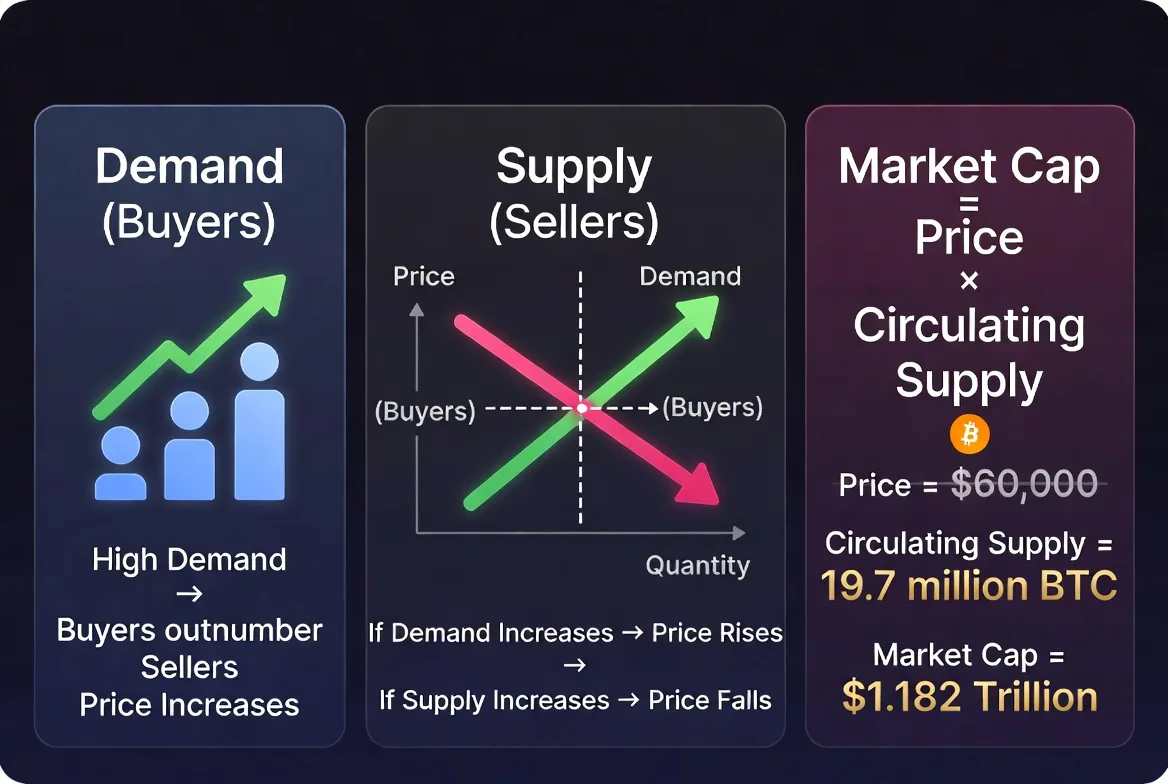

Cryptocurrency derives its value from the same fundamental force that determines the price of any asset: supply and demand. When more people want to buy Bitcoin than sell it, the price rises. When sellers outnumber buyers, it falls. This dynamic plays out across thousands of exchanges worldwide, with prices adjusting continuously based on the last completed transaction.

Market capitalization—the total “value” of a cryptocurrency—is calculated by multiplying the current price by the circulating supply. If Bitcoin trades at $50,000 and 19.5 million coins are in circulation, the market cap equals $975 billion. This calculation creates a critical illusion: it assumes every single coin could be sold at the current price, which is never actually possible.

Understanding crypto market cap requires recognizing that it represents theoretical value, not actual dollars invested. The market cap figure answers the question: “What would all these coins be worth if we could sell them all at today’s price?” But attempting to sell them all would immediately crash the price, revealing that this theoretical value doesn’t reflect real money sitting anywhere.

Value in crypto explained comes down to collective belief and utility. Bitcoin has value because people believe it will remain scarce (21 million coin limit), that it provides censorship-resistant transactions, and that others will continue wanting it. Ethereum has value because developers build applications on it, creating demand for ETH to pay transaction fees. This belief-based valuation makes crypto particularly vulnerable to sentiment shifts—when confidence evaporates, so does price.

The price you see on any exchange reflects only the most recent transaction between one buyer and one seller. If someone sells 0.1 Bitcoin for $5,000, that sets the “market price” at $50,000 per coin—even though only $5,000 actually changed hands. This price then gets multiplied by millions of coins to calculate a market cap in the hundreds of billions.

What Actually Happens During a Crypto Market Crash

Crypto market crashes follow predictable patterns driven by liquidity constraints and psychological factors.

A crash typically begins when a catalyst—regulatory news, exchange failure, macroeconomic shift, or technical breakdown—prompts significant holders to sell. These initial sales push prices down, triggering stop-loss orders (automatic sell orders set at predetermined prices). As these automated orders execute, they create additional selling pressure, pushing prices even lower.

What happens to crypto value in a crash accelerates through cascading liquidations. Traders using leverage (borrowed money) face forced liquidations when their collateral value drops below required thresholds. Exchanges automatically sell these positions to recover loaned funds, creating waves of selling unrelated to individual decision-making. During the May 2021 crash, over $8 billion in leveraged positions were liquidated within 24 hours, amplifying the price decline.

Crypto panic selling effects compound as fear spreads. Investors who might have held through a 10% decline start selling at 20%, then 30%. Social media amplifies anxiety, with crash-related posts increasing exponentially as prices fall. The psychological pain of watching unrealized gains evaporate often overwhelms rational analysis, converting patient holders into panicked sellers.

Order books—the lists of buy and sell orders at various prices—thin out dramatically during crashes. Under normal conditions, substantial buy orders exist at prices slightly below market, providing support. During panics, these buyers disappear or drastically lower their bids. A cryptocurrency trading at $100 might have buy orders totaling $50 million between $95 and $100 during calm periods. In a crash, those orders vanish, leaving the next significant buy order at $80 or $70.

Crypto liquidity in downturns becomes scarce precisely when it’s most needed. Liquidity—the ability to buy or sell without dramatically affecting price—evaporates as market makers widen spreads and reduce position sizes. A coin that normally trades with a 0.1% spread (difference between buy and sell prices) might see spreads widen to 2% or more, making transactions more expensive and further discouraging trading.

The price discovery process during crashes happens in rapid, discontinuous jumps. Rather than smoothly declining, prices often gap down—jumping from $100 to $92 with no trades in between. These gaps occur when all buy orders at intervening prices get filled or cancelled, forcing sellers to accept progressively lower bids.

Where the Money Goes When Crypto Prices Fall

The core answer to “if crypto crashes where does the money go” challenges common assumptions: most of the “lost” money never existed as cash in the first place.

When Bitcoin’s market cap drops by $100 billion, it doesn’t mean $100 billion in cash left the crypto ecosystem. Instead, it means that the collective theoretical value of all Bitcoin—calculated by multiplying the current price by total supply—decreased by that amount. The actual cash that changed hands might be just a few billion or even less.

Consider a simplified scenario: A cryptocurrency has 100 million coins. At $10 per coin, its market cap is $1 billion. If just 1 million coins (1% of supply) sell for $8 each, the new market cap becomes $800 million—a $200 million “loss.” But only $8 million in actual cash moved (1 million coins × $8). The remaining 99 million coins simply became worth less on paper, but no money actually left those holders’ wallets until they sell.

Money flow out of crypto during crashes follows several paths:

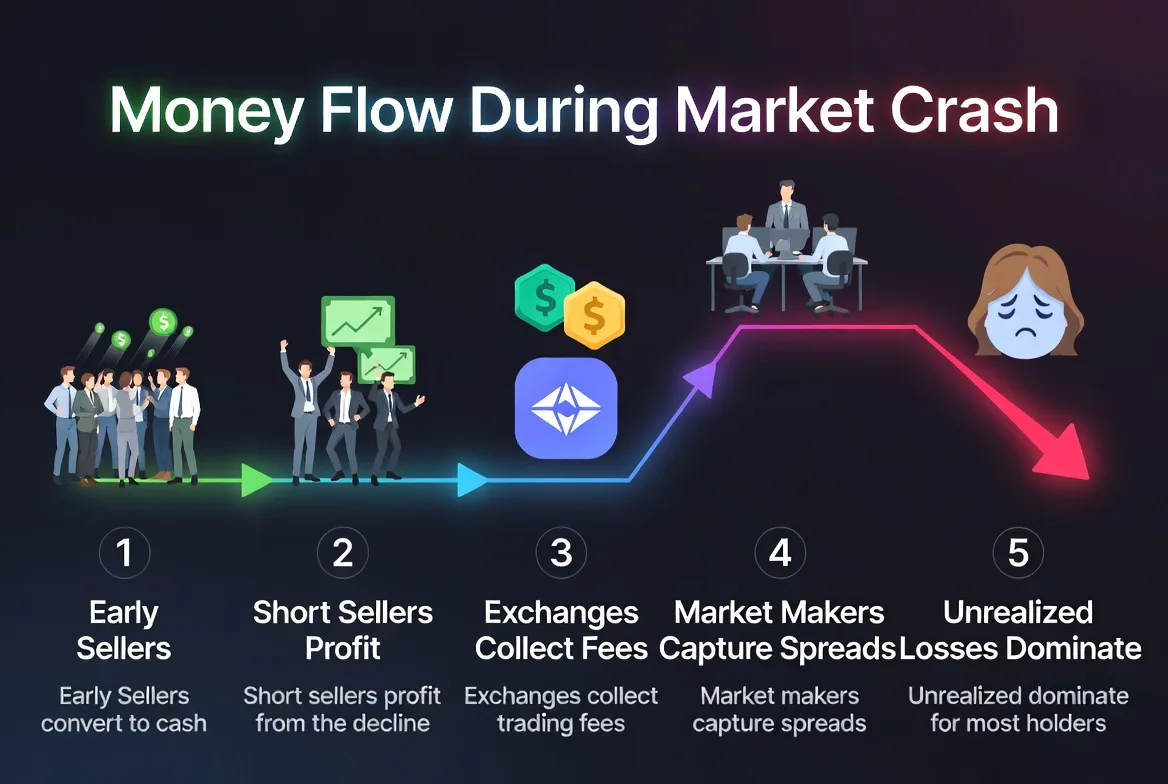

Early sellers capture real value. Investors who sell near the top convert their paper gains into actual dollars. If you bought Bitcoin at $20,000 and sold at $60,000, you extracted $40,000 in real profit per coin. That money came from the buyers who purchased at $60,000, believing prices would continue rising.

Short sellers profit from declines. Traders who bet against cryptocurrencies by borrowing coins, selling them, then buying back at lower prices to return them, capture the difference as profit. When Bitcoin drops from $50,000 to $40,000, a short seller might profit $10,000 per coin. This represents wealth transfer from long holders to short sellers.

Exchanges collect fees regardless. Whether prices rise or fall, exchanges charge transaction fees. During high-volume crashes, exchanges often generate substantial revenue from panic trading, though they don’t “get” the lost market cap.

Liquidity providers and market makers capture spreads—the difference between buy and sell prices. During volatile crashes, these spreads widen significantly, allowing sophisticated traders to profit from providing liquidity to panicked sellers.

The critical insight: crypto money movement during crashes is primarily a revaluation rather than a transfer. Imagine you own a rare painting appraised at $1 million. If similar paintings start selling for $500,000, your painting’s “value” dropped by $500,000—but no money actually moved. The $500,000 loss exists only when you sell at the new price. Until then, it’s an unrealized loss, reflecting changed market perception rather than actual cash flow.

Most money “lost” in crypto crashes represents the evaporation of unrealized gains—profits that existed on paper but were never converted to cash. If you bought Ethereum at $100, watched it rise to $4,000, then crash to $1,500, you didn’t “lose” $2,500 per coin in actual money. You lost potential profit, but your original $100 investment still grew 15x.

The Difference Between Market Cap and Real Money in Crypto

The confusion between market capitalization and actual invested capital causes widespread misunderstanding about crypto market cap destruction.

Market cap is a multiplication exercise: current price × circulating supply. It measures theoretical total value but tells you nothing about how much cash people actually invested. A cryptocurrency could have a $10 billion market cap with only $500 million in actual dollars invested over its history.

“Realized cap”—a metric that values each coin at the price it last moved rather than current market price—provides a more accurate picture of actual invested capital. During the 2021-2022 crash, Bitcoin’s market cap fell from approximately $1.3 trillion to $320 billion (a $980 billion drop), while its realized cap declined from roughly $450 billion to $380 billion (a $70 billion drop). This disparity reveals that most “lost” value was unrealized gains rather than actual invested money.

Market Cap vs. Actual Money: A $100 Billion Crash Example

| Scenario | Market Cap Change | Actual Cash Moved | Where Value Went |

|---|---|---|---|

| Pre-crash baseline | $500 billion (50M coins @ $10,000 each) | N/A | Theoretical value based on last trade |

| Initial 10% drop | -$50 billion (price falls to $9,000) | ~$2 billion in sales | Early sellers extracted cash; remaining holders have unrealized losses |

| Cascade to -30% | -$150 billion (price falls to $7,000) | ~$6 billion total sales | Liquidations and panic selling; short sellers profited; most loss is paper value evaporation |

| Partial recovery +10% | +$35 billion (price rises to $7,700) | ~$3 billion in purchases | Buyers at bottom paid cash to sellers; market cap increases with minimal cash input |

This table illustrates how massive market cap swings require relatively modest actual cash movement. The “lost” $150 billion in the crash scenario didn’t go anywhere—it simply ceased to exist as perceived value.

Understanding crypto market cap requires accepting that it’s a sentiment indicator rather than a measure of money in the system. When enthusiasm is high, market cap inflates rapidly with minimal capital inflow. When fear dominates, it deflates just as quickly with minimal capital outflow.

The lost capital in crypto crash scenarios is mostly opportunity cost—the difference between what you could have sold for at the peak versus what you can sell for now. Real capital loss only occurs when you actually sell at a lower price than you bought, converting paper losses into realized losses.

Money Flow Patterns During Crypto Downturns

Tracking actual capital movement during downturns reveals where money genuinely flows rather than where value appears to vanish.

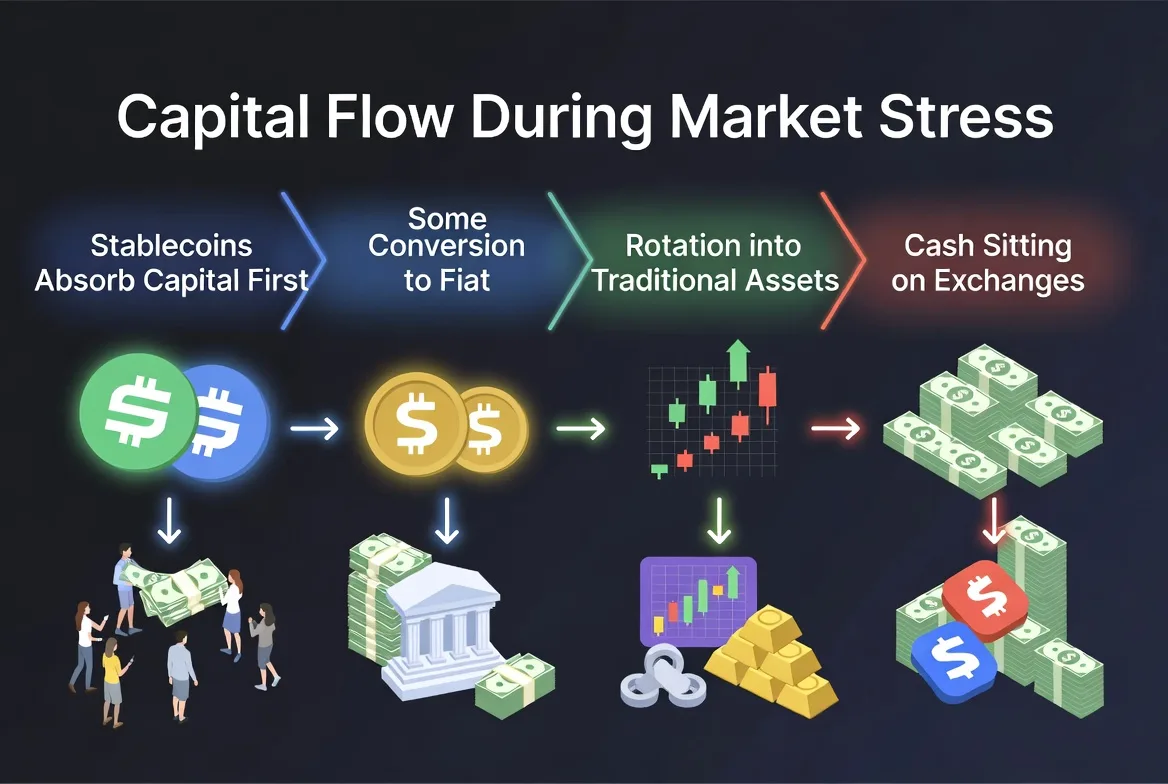

Flight to stablecoins represents the most common initial movement. Rather than converting crypto to dollars and leaving the ecosystem entirely, many investors sell volatile assets for stablecoins like USDC or USDT. This preserves capital in crypto-friendly form while avoiding further downside. During the 2022 downturn, stablecoin market cap remained relatively stable around $150 billion even as total crypto market cap plummeted, indicating significant capital rotation rather than wholesale exit.

Conversion to fiat increases as crashes deepen. Investors who initially moved to stablecoins often eventually withdraw to bank accounts, particularly if they need funds for expenses or lose faith in crypto entirely. This represents genuine money flow out of crypto, though even here the amounts are smaller than market cap declines suggest.

Rotation into traditional assets captures some capital. Investors might sell crypto to buy stocks, bonds, real estate, or gold. This represents portfolio rebalancing rather than value destruction—the money doesn’t disappear, it just moves to different asset classes.

Sitting on exchanges describes substantial capital that doesn’t actually leave. Many investors sell their crypto but leave the cash in exchange accounts, waiting for buying opportunities. This money remains in the crypto ecosystem, ready to re-enter markets.

Why Some Investors Profit While Others Lose

Crypto markets aren’t perfectly zero-sum (exchanges and miners extract ongoing value), but they contain strong zero-sum elements during crashes. Your loss often represents someone else’s avoided loss or outright gain.

Timing determines outcomes. If you bought Bitcoin at $60,000 and sold at $40,000, you lost $20,000 per coin. The person who bought from you at $40,000 and later sold at $50,000 gained $10,000 per coin. The person who bought your coins at $60,000 and held through the crash to $40,000 has an unrealized loss of $20,000 per coin. These interconnected outcomes show how value transfers between participants based on entry and exit timing.

Liquidity providers profit from volatility. Sophisticated traders and automated market makers capture spreads between buy and sell prices. When panic selling widens these spreads from 0.1% to 2%, market makers can profit substantially by providing liquidity. Your 2% loss to the spread becomes their 2% gain.

Short sellers explicitly profit from others’ losses. When you hold a coin that drops 40% in value, short sellers covering their positions at these lower prices directly profit from the decline. This represents a clear transfer of wealth from long holders to short sellers.

Information asymmetry matters. Investors with better information, faster execution, or superior analytical tools consistently extract value from less-informed participants. When major holders know about impending negative news before the public, they can sell at higher prices, transferring losses to later sellers.

The uncomfortable reality: in every crash, some participants capture real value while others absorb real losses. The aggregate “lost” market cap vastly exceeds actual wealth transfers, but genuine winners and losers exist within that broader illusion.

Common Misconceptions About Lost Value in Crypto

Several persistent myths about lost capital in crypto crash scenarios deserve correction.

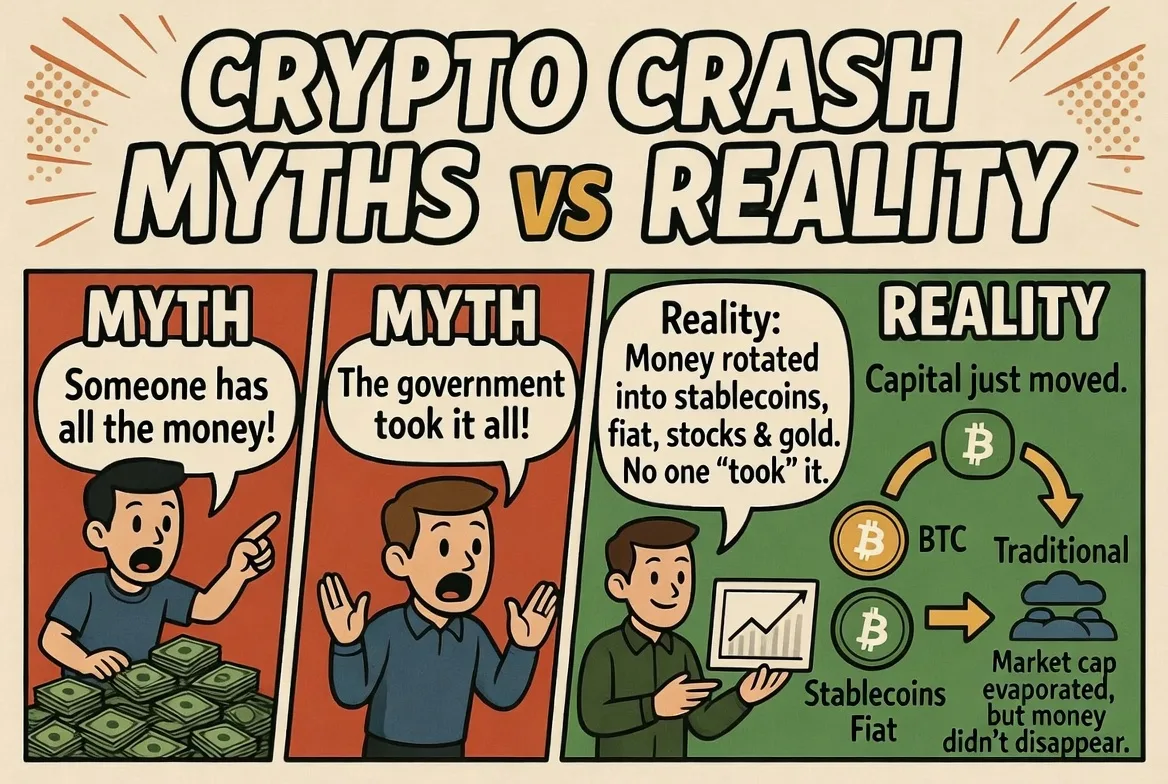

Myth: “Someone must have all the money that disappeared.” Reality: Most “lost” value never existed as money. When market cap drops $500 billion, there’s no vault somewhere containing $500 billion that transferred from crypto holders to someone else. The vast majority represents revaluation of assets that people continue holding.

Myth: “The government or banks took the money.” Reality: While governments collect taxes on realized gains and banks charge fees for fiat transactions, they don’t capture market cap declines. The government doesn’t profit when your unrealized crypto gains evaporate—they only tax actual profits when you sell.

Myth: “It’s all a scam designed to take your money.” Reality: While crypto certainly contains scams, market cap destruction during legitimate crashes isn’t a scam—it’s how all markets work. Stock markets, real estate, and commodities experience the same phenomenon where small selling pressure creates large market cap declines.

Myth: “Crypto crashes prove it has no real value.” Reality: Volatility and value are separate concepts. Many valuable assets experience significant price swings. Crude oil, a commodity with obvious utility, has seen 70%+ crashes. Price volatility reflects uncertainty and speculation, not absence of underlying value.

Myth: “Early Bitcoin buyers have all the money.” Reality: Early buyers who sold captured significant gains, but many held through multiple boom-bust cycles, experiencing massive unrealized gains and losses. Some early holders lost access to their coins entirely. The notion that a specific group “has” all the lost value misunderstands how market cap works.

Myth: “Market cap equals money invested.” This fundamental confusion underlies many others. Market cap never equaled invested money. It’s always been a theoretical calculation based on the most recent trade price multiplied by total supply. Recognizing this distinction eliminates most confusion about where money “goes” during crashes.

Market capitalization is not the same as the amount of capital that went into an asset. A relatively small amount of buying or selling can result in large changes to market capitalization, because market cap is calculated by multiplying the current price by the number of units, even though most of those units haven’t actually traded at that price.

Lyn Alden

FAQs

No, not directly. When your crypto loses value in a crash, your money doesn’t transfer to another person’s account. Instead, the theoretical value of your holdings decreases based on what buyers are currently willing to pay. Your loss becomes someone else’s gain only if you sell at a low price and they later sell higher, or if short sellers profited from the decline. Most “lost” value simply evaporates as unrealized paper gains rather than transferring to specific individuals.

If you buy crypto with your own money (not borrowed funds), you can only lose what you invested—your loss is capped at 100% if the coin becomes worthless. However, if you trade with leverage (borrowed money) or margin, you can lose more than your initial investment. For example, if you invest $10,000 and borrow another $40,000 to control $50,000 worth of crypto, a 25% price decline wipes out your $10,000 and leaves you owing money to cover the loan. Always avoid leverage unless you fully understand the risks.

The money in crypto exists in different forms. Cash you originally invested was real money that you exchanged for cryptocurrency. Any gains since then are “on paper” until you sell—they represent current market value rather than cash in hand. When you successfully sell crypto and withdraw dollars to your bank account, those gains become real money again. Until that point, your crypto wealth is theoretical, subject to market fluctuations. Many people confuse paper wealth with actual cash, leading to poor decisions during volatility.

When Bitcoin crashes, the “money” doesn’t go anywhere because most of it never existed as actual currency. Bitcoin’s market cap (price × supply) drops dramatically, but this represents a revaluation rather than money movement. Small amounts of actual cash flow from panic sellers to buyers at lower prices, from long holders to short sellers who profit from declines, and to exchanges as trading fees. The vast majority of “lost” value is simply unrealized gains that evaporate—potential profits that existed on paper but were never converted to cash.

Market cap drops more than actual withdrawals because it’s calculated by multiplying the current price by total supply, assuming every coin could sell at that price. In reality, selling even a small percentage of supply drives prices down significantly, which then reduces the calculated value of all remaining coins. If 1% of Bitcoin supply sells at 10% below the previous price, the entire market cap drops by 10%—not just the 1% that traded. This multiplier effect explains why $1 billion in selling can cause $50 billion in market cap decline.

Understanding where money goes when crypto crashes requires distinguishing between market capitalization changes and actual cash movement. The vast majority of “lost” value during crashes never existed as money—it was always theoretical worth based on the last trade price multiplied across all coins.

Real money flows from sellers to buyers, from long holders to short sellers, and to exchanges as fees. But these flows represent a fraction of the market cap declines that dominate headlines. When Bitcoin’s market cap drops by $200 billion, perhaps $10-20 billion in actual cash changed hands, with the remainder representing evaporated paper gains.

This distinction matters for managing your own crypto investments. Unrealized gains aren’t real money until you sell. That portfolio worth $100,000 at the peak only becomes actual money when you convert it to dollars in your bank account. Until then, it remains exposed to market revaluations that can dramatically reduce its theoretical worth.

The money didn’t go anywhere because it was never really there—it was always a collective belief about value that could change instantly. Recognizing this reality helps you make better decisions about when to realize gains, how much volatility you can tolerate, and whether crypto’s risk-reward profile suits your financial goals. Markets don’t destroy money so much as they reveal which values were always illusory.